THE FUTURE OF RETAIL.

one retail: convergence and human touch.

LINKEDIN article, February 27th 2019

Where is retail headed? A lot has been said already about the future of brick-and-mortar retail, e-commerce prevalence, and the destiny of trade at large. But here’s a take on it.

Granted, consumer technology has been disruptive (mostly in its mindset) and is here to stay.

E-commerce has been growing in all categories and services, often taking advantage of physical businesses weaknesses (high rents, personnel costs, inventories inefficiencies, lack of innovation) and being able to shiftily recognize, accept and metabolize changes in the world and in customers’ needs.

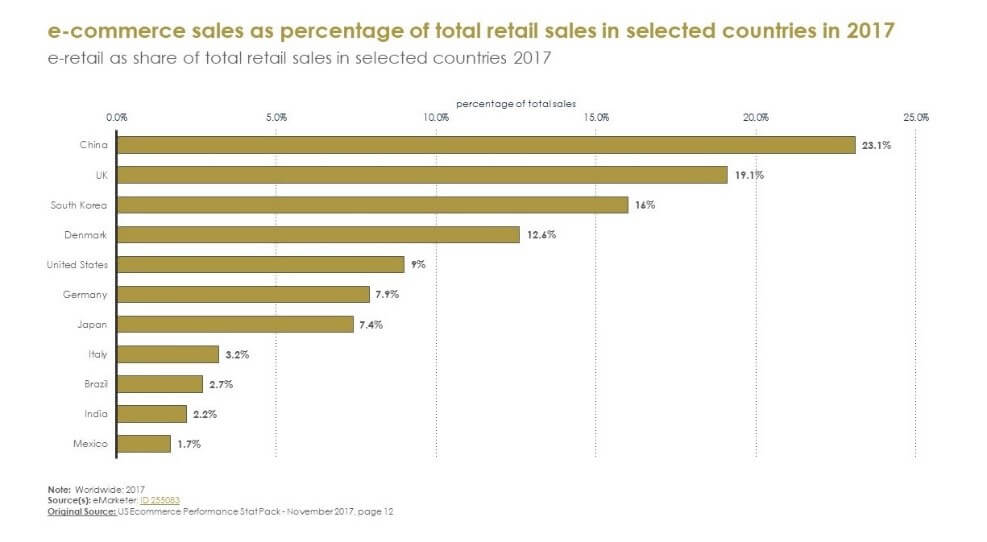

Nevertheless, it still represents a limited percentage of the total retail sales.

In China, the country that has enthusiastically embraced e-commerce more than any other in the world. In 2017, e-commerce represented the 23.1% of total retail sales, compared to19.1% in the UK, 9% in the US, 7.4% in Japan and 2.2% in India.

That said, e -commerce and digitally native brands are far from taking over, and, in fact, are actively trying to find new customers and audiences. Due to surges in acquisition costs, they are increasingly expanding into physical retail, snapping locations left empty by closing brands.

This means that a growing number of digital-native and physical-native brands are operating in the same space, CONVERGING INTO ONE even more sophisticated omnichannel RETAIL.

Within this scenario, undoubtedly, physical brands and retail businesses need to embrace e-commerce and digital channels to reply to savvy customers’ expectations of ‘seamless’ shopping experiences.

Nevertheless, the upgrading of infrastructures alone does not seem to be a strong enough answer to this competitive environment.

For physical and digital organizations alike, the capacity to continue to thrive is likely to have more to do with the ability of managing (hopefully profitably) diverse and synchronized business models and, most importantly, impeccably delivering consistent CONTENT and SUBSTANCE in products and services.

To preserve content, there is probably value in going back and review the basics: the analog, human side of the business that seem to have been curiously forgotten in a market smitten by financial efficiency and all technology is promising to offer.

Brands and platforms may consider re-focusing on markers that define the appeal and consistency of products and services as:

A correct management of these aspects NATURALLY results into tangible and authentic experiences at the intersection of physical and digital channels. There is no need for gimmicks if the basics are in place.

Food has been doing this best, providing well organized environments that give space to a community of experts and craftsmen — stakeholders who proudly share their direct knowledge with customers.

Think Japanese supermarkets, grocery pioneers PECK and EATALY and, the latest, HEMA with its seafood market; retail companies that have created a brand providing high quality products and culinary experiences with knowledge.

There is a large amount of relevant, invaluable content lying around, the culture companies created through decades that just in need of re-invigoration and to be communicated within the new the omnichannel context that great technology and a new mind set can facilitate.

As said by Fajrin Rasyid, co-founder of BUKALAPAK, we should engage in ‘coopetition‘.

“It is true that we can compete with other businesses in some aspects, but it does not mean that we cannot collaborate in other aspects. Hence, instead of treating everyone as enemies, I suggest businesses to have mindset of “always think what potential collaboration we can have with other parties”.

Digital and physical brands and platforms will benefit re-discovering their analog value, while accepting and learning from each other.

To survive the future, human touch-tech integration and convergence are a must.