CURRENT. POINT. beyond branding.

We came across an article in the Straits Times about ‘Isetan’s tale of two cities’ that, ironically, suggests additional input on how we look at the current issue in commerce.

The discussion about a retail brand globalization in the article – by Isetan – is quite contemporary and functions as a pretext to argue for a fuller, less comforting analysis about how to look at and requalify traditional business models in practice beyond the narrative of branding.

The expectation that Isetan Orchard, the last remaining shop of the Isetan group in Singapore, could successfully align with—or in part evoke—the same brand prestige and aura that the Shinjuku Main Store commands is fundamentally unrealistic, given the current commercial landscape on the island and in other cities. It would be equivalent to expecting that Isetan Kyoto or other national branches would be on the Shinjuku’s same level as well. Which, as many know, is not the case at all.

Why is this not the case, and is this an issue of branding, or branding alone?

WHAT. IS WHAT. While often confused with and used synonymously, department stores and malls are distinct retail formats. It is important to understand their difference in interpreting the demise of department stores in certain markets rather than others.

A DEPARTMENT STORE is a large, single establishment offering a wide range of goods organized into departments (e.g., fashion, cosmetics, homeware, food). The operator (the chain itself) centrally controls purchasing, merchandising, pricing, staffing, and curation to deliver a cohesive, one-stop mid- to high-end shopping experience with a strong emphasis on quality and service.

A MALL is an enclosed complex of multiple independent stores, restaurants, entertainment, and services, often anchored by department stores. The operator (developer, REIT, or management firm like CapitaLand) acts as landlord and coordinator: renting units, curating a tenant mix , managing common areas, marketing, events, and maintenance—without owning inventory or handling product merchandising – tenants manage their own operations.

There are different types of malls. A strata mall (common in Singapore) is a multi-level complex with individual units sold and owned separately under strata title, leading to fragmented ownership. A management corporation (MCST) serves as limited operator, handling only maintenance fees, shared services, and basic rules. It lacks control over tenant mix or curation, resulting in eclectic tenants, lower rents, coordination challenges, but greater individual owner agency, agility as well as diversity in products and services.

In contrast, malls like PARCO in Japan maintain a leasing structure while emphasizing strong market positioning, coordinated cultural content, and trend-focused curation (e.g., fashion innovation, art events, youth/lifestyle concepts), creating a more unified, experiential destination despite relying on independent tenants.

Finally, to adapt to rising costs, e-commerce, and market shifts, many department stores now use a MIXED MODEL, combining centrally bought/owned inventory with concessions – leased brand spaces where brands control their own stock and merchandising while paying rent/commissions. Isetan embraced this model a few decades ago.

COUNTRY LEVEL. DISTRICT. DIFFERENCES & LOCALIZATION. As suggested in the article, a global premium brand may – and we may add MUST – adopt different brand positioning, mix, and product portfolios across markets. It may also need “to adjust its strategy over time, particularly when strong local competitors dominate overlapping market segments”.

Markets vary within the same territory, let alone across countries.

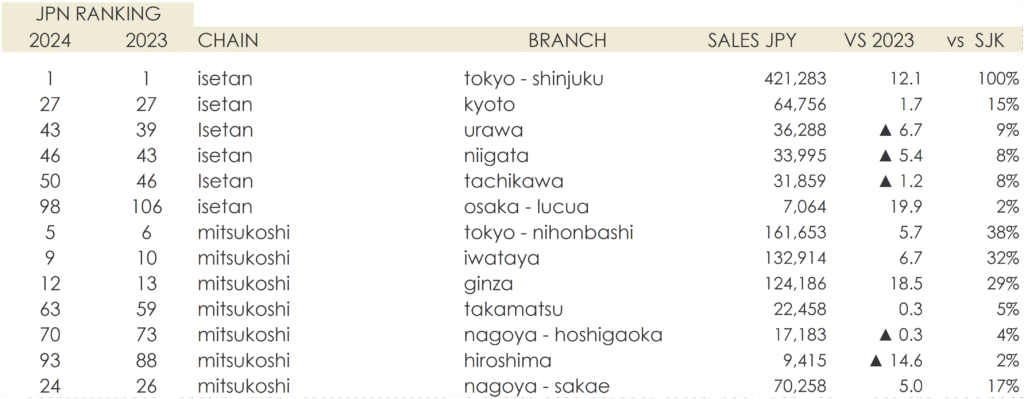

Isetan Shinjuku main store is very different not only from its overseas sister shops but also from all the other branches in the country. Based in the biggest city of the country that attracts the largest number of visitors, it is by far the leading group performer. It is the crown jewel rather than the complete expression of the group, an anomaly.

Isetan Orchard sales in 2023 – prior to delisting – were S$84.28 million or about 65 USD million at today rates. Further sales data is not available.

Isetan-Mitsukoshi group Sales for the fiscal year 2025 are not yet available and will be published after the end of the fiscal year in March. In 2024, Shinjuku Isetan sales were about ¥421 billion, equivalent to approximately S$3.42 billion or US$2.66 billion at today’s rates. The second-strongest shop of the group – Nihonbashi Mitsukoshi, strongly patronized by local regular customers – reached sales equal of about 38% of Shinjuku.

National branch-level sales in the same year are significantly different.

CONSUMER. LOCAL MARKET & UNDERSTANDING. Such divergent performance across national markets suggests that customer profiles and shopping propensities deeply influence outcomes. A profound understanding of local consumers is essential—and must, we add, first and foremost, have realistic applications.

As the article suggests, Singapore’s “efficiency-driven consumers often shop opportunistically”. They are highly sensitive to price positioning and currency fluctuations, frequently shopping abroad – including in Tokyo – or online. This suggests difficulty with product/service alignment.

Moreover, the contribution of foreign tourists to shop sales—and therefore their weight in overall performance—differs dramatically between Isetan Shinjuku and Isetan Singapore, both in absolute terms and in potential. Shinjuku benefits greatly from Tokyo’s status as a global tourism hub, attracting high-spending international visitors who drive demand for luxury, fashion, and gourmet products.

It would be a mistake not to consider how the weakening of the yen has resulted in a surge in inbound tourism – weak yen making Japan a bargain for foreigners and Asia. The growth of Shinjuku Isetan has, although not in proportion, been fuelled by the differential in prices created by a weaker yen and duty-free, as well as by different brands’ price positioningversus China.

Singapore’s department stores rely less on inbound tourism for sustained volume than their Japanese counterparts, which amplifies the impact of local consumer behaviour.

Certainly, the curation of offerings has not been up to standard in recent years. A decisive change in the shop content and merchandising offerings is needed and seems to have been timidly re-ignited more recently after the consolidation, in view of the decrease in future losses.

Isetan Orchard has an excellent food floor with loyal customers, many of whom have probably patronized other floors and could be further converted into overall patrons of the building, although it might prove hard to convert them all.

Of course, it would be ideal if more services and a diverse range of offerings could be included. Think of a restyling of the basement, a reconfiguration of floors, a robust incorporation of wellness and lifestyle, now trending as vehicles for diverse traffic and core ‘experiences’.

But how to make it viable?

Isetan is not alone in facing these challenges: Robinsons, BHG, Metro, and other legacy department stores have encountered similar—or even more severe—challenges, many resulting in full closure or drastic downsizing.

What are the other elements hindering the success of Isetan?

SIZE. OWNERSHIP. & MARGINS. Isetan Singapore extends on about 8,800 square meters, a cry from the roughly 60,000 square meters of its Shinjuku counterpart. It is a contemporary ‘large’ store. Shinjuku is effectively 7–8 times larger or more in usable retail space, enabling far greater assortment, experiential zones, and sales density.

Ownership structures further exacerbate the contrast. Isetan Shinjuku operates in a property fully owned by Isetan Mitsukoshi Holdings, granting complete control over remodeling, tenant mix (in adjacent areas), and long-term cost stability—there are no external rent pressures to erode margins.

Isetan Orchard rents its premises from Shaw Centre. While Shaw is not part of a REIT and therefore unlikely to expose Isetan to significant market-rate fluctuations, it is likely that rates have been a sensible burden in the last few years, together with losses in the periphery and sales, reducing operational marginality.

This structural gap—size for scale economies, ownership for cost control, and resulting margin resilience—needs consideration.

CONTENT & PROXIMITY. One of the decisive factors in Isetan’s divergent trajectories has been the need to deeply understand—and adapt to—the local consumer reality and the immediate neighbourhood ecosystem, which largely outweighs the brand’s own global identity ‘DNA’ in determining viability.

In Shinjuku, the flagship strategy has centered on elevating the content and merchandising offering in a fragmented urban district where an uneven architectural landscape has limited many luxury brands’ ability to establish a strong street-level presence. By curating an exceptional mix of concessions and exclusive offerings, Isetan Shinjuku has become a concentrated, high-value destination that captures a significant share of sales through selected brand partnerships. This approach thrives precisely because the store serves as the primary showcase in a dense district.

Orchard Isetan does not sit in the same position. It probably started with that intention, but it needed to face its own ‘reality’ – size, financials, customer, and the rising competition developing in Orchard Road through the years. Let’s remember Lane Crawford and On Pedder, Tangs, Robinsons and Ngee Ann City, Paragon and Marina Bay Sands among the others.

Brands’ presence is already saturated in Orchard, where brands can have larger store fronts as well as different economic conditions in CapitaLand, Ngee Ann City, or Paragon.

Tourist dynamics add another layer of divergence. While Singapore attracts substantial inbound visitors, the absolute volume—and especially the concentration on Orchard Road—does not match Tokyo’s scale in recent years. in addition, tourist spending is increasingly fragmented across an “over-shoppified” area.

So, the content can’t be the same, and – here we agree – needs to be strategic.

THE SIN. The “original sin” of many department stores has been moving too quickly into peripheral and foreign markets—often in partnership with developers and landlords—expecting to find demand in a sector of the market similar to the domestic one, only to realize the challenges and ‘adapt’ the models to those markets late in their history, when other players had already occupied the space they could have morphed into.

Undoubtedly, in Isetan’s case, there could have been some degree of ‘rigidity’ in the original development approach that is, however, typical of the mandate to maintain and preserve the ‘brand’ culture.

From this perspective, digital was not adequately addressed at home or abroad–this lag compounds the challenge in a market where online convenience increasingly dominates today. The product curation was initially better and has at times been mistakenly shrunk probably due to a literal interpretation of sales results – read need of sales – without leaving room for potential growth. In this regard,It acknowledged and tried to incorporate Singapore’s local cultural connections. However, Isetan seem to have recognized that it had faced significant challenges in its expansion and mistakes in underestimating the peripheral markets.

All things considered, however, it would be unfair to suggest that the story could have been much different.

Reflecting on Isetan’s misfortunes in markets such as Singapore gives us an opportunity to ask ourselves what the real picture is: whether there are simply too many stores, whether Orchard is overserved by redundant concepts relative to the local customer base, and whether there is a critical mass of patrons interested in the price positioning of those brands that could pay the rents required to sustain the existing malls in a relatively small district.

And if not, what would be the content formula, the model that could allow entities like Isetan Orchard to excel? If shopping patterns have changed, does the way we organize the commercial offer need to reflect that?

What do we export when we export a retailer brand? See also Harrods’ recent closure in China.

Which part of know-how must be transferred?

We live in a new world and a retail landscape that has changed. It is evident that, beyond narrative, commercial presence must have meaning and a function.

We need to face facts while being honest about the market and what it needs. Not all cities need to be the same, nor do they need the same shops. Not all branches need to be the same: Orchard is not Shinjuku, nor should it try to be. It is already saturated with too many brands—over-served and redundant for the actual local customer base.

Actually, the opportunity lies here—in Orchard’s reality.

Isetan should return to its curatorial roots and build a new—not brand-based—concept that delivers the differentiation and diversity the market is asking for, rather than trying to duplicate a model that succeeded elsewhere but is not sustainable in this time.

In the end, branding and marketing remain powerful tools: they shape perception, build emotional connections, and differentiate a retailer’s communication in crowded markets.

Yet, as this case shows, if the fundamentals—market realities, competition, quality and value proposition, scale, ownership control, and structural viability—are missing or misaligned, branding and marketing efforts become merely aspirational, unable to sustain what lacks meaning or economic grounding.

Retail sustainability and differentiation start not with a narrative, but with an honest ground acknowledgement.

ABOUT THE ARTICLE DISCUSSED HERE.

A tale of two cities, two Isetans and a retail conundrum

https://www.straitstimes.com/opinion/a-tale-of-two-cities-two-isetans-and-a-retail-conundrum